Identity Proofing: What It Is, How It Works, and Why It’s Essential

You must have once opened a bank account entirely online, or registered on a government portal or signed up for a FinTech app – all without setting foot in an office. But how do these platforms really know who you are, and why do they trust you? Well, they all use “identity proofing” – a method to verify that a person is who they say they are before granting access to a service.

Identity proofing helps prevent fraud, ensures compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations, and keeps digital onboarding smooth yet secure. Let’s break down what it is, how it works, and why it’s crucial for businesses today.

What is Identity Proofing?

Identity proofing is the process of verifying that a person’s claimed identity corresponds to a real individual using trustworthy evidence, such as a government ID (passport, driver’s license), biometrics (your face or fingerprints), or authoritative data (credit bureau or government databases). All those pieces of evidence are collected and evaluated to ensure your claimed identity matches your actual identity, validated by official documents and records.

Unlike simple login verification – entering a password or an SMS code, identity proofing tends to happen once at onboarding or account creation, to establish your identity initially. It builds a foundation of trust and establishes a verified link between your physical identity and your digital one.

In 2023 alone, Americans lost over $43 billion to identity fraud schemes affecting some 15 million people.

As the US National Institute of Standards and Technology ‘s (NIST) Digital Identity Guidelines (SP 800-63A) describe, proofing involves “resolving, validating, and verifying identity evidence to a defined level of assurance.” In other words, it ensures that you are you, and not a fraudster pretending to be you.

The Identity Proofing Process

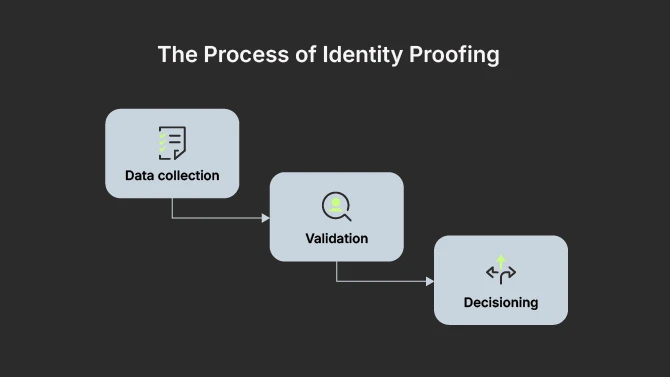

Every identity proofing process follows three core steps: data collection, validation, and decisioning.

1. Data Collection

This step establishes a “claimed identity” that the system will test. At this stage, the user submits personal and biometric data, like a driver’s license scan, a selfie, and key details such as full name or date of birth. For example, when you sign up for an online bank account, you might upload your passport and record a short selfie video.

2. Validation

During this step, the system checks if the provided evidence of a person’s identity is genuine.

- Scans documents for authenticity features (holograms, fonts, chip data).

- Performs a biometric match by confirming that the selfie matches the ID photo and that it’s a live person (not a photo of a photo).

- Cross-verifies data with government databases or credit records.

3. Decisioning

The system aggregates validation results to produce a risk score or confidence level, based on which it decides whether to approve, reject, or flag the identity for manual review.

A well-designed process achieves what NIST calls identity assurance: the confidence that “this identity truly exists and belongs to this person.” NIST’s guidelines define Identity Assurance Levels (IAL1, IAL2, IAL3) for different rigor in proofing.

Identity Proofing vs. Identity Verification

These two terms are often mixed up, and usually go hand in hand, but they serve different purposes.

- Identity proofing is the process of verifying an individual is who they claim they are when they first interact with an organization. It involves collecting and validating identity-related information to establish a person’s identity before they can access services or complete transactions. It focuses on the authenticity of data provided during the onboarding or account creation processes.

- Identity verification helps ensure the person presenting the information is the rightful owner of that identity. This process can involve various methods, such as device intelligence, Knowledge-Based Authentication (KBA) questions, biometric verification, and Multi-Factor Authentication (MFA).

Understanding the difference between these two terms helps clarify that initial trust must be established through proofing and then maintained over time through identity verification. If you proof someone’s identity strongly at account creation, all subsequent verifications (logins, etc.) are built on a solid foundation.

Identity Proofing and Authentication

Now, where does authentication come into play in all this? It’s easy to confuse authentication with identity proofing, because both involve confirming identity. But they occur at different stages of the user journey and use different methods.

Proofing happens once to establish that your identity is legitimate. Authentication happens every time you log in to prove it’s still you.

In essence, identity proofing is usually a precursor to identity authentication. The authenticating methods include:

- Passwords or PINs – a classic “something you know” factor.

- 2FA or OTPs – combines “something you know” (password) with “something you have” (a one-time code generator app or an SMS to your phone) or “something you are” (biometric).

- Biometrics – a “something you are” factor that uses your fingerprints, face (Face ID), or voice to authenticate, often used in combination with a device security measure (your phone’s fingerprint).

Without strong proofing, even perfect authentication can fail, because you might just be authenticating a fraudulent account. That’s how proofing and authentication work together to build a trusted identity lifecycle.

In summary, identity proofing and authentication are two sides of the identity security coin. Proofing means enrollment – one-time rigorous verification of identity, establishing trust. Authentication means access control – repeat verifications to maintain trust each time the user accesses.

Identity Proofing Services and Technologies

Modern identity proofing relies on a mix of advanced technologies, many of which are powered by AI, to verify identities quickly and accurately.

Biometric Verification

Biometric verification identifies you via facial recognition, fingerprints, or voice. During proofing, you typically take a selfie that’s matched against your ID photo. Liveness detection is crucial in biometrics: it confirms you’re a real person, not a photo or video spoof, by asking you to blink or turn your head. Biometric data ensures the person is real and matches the claimed identity, and is a strong weapon against stolen passwords or forged documents.

According to NIST, top facial recognition algorithms now exceed 99% accuracy in controlled settings, though privacy and bias must be carefully managed.

Document Scanning and NFC Reading

Government IDs contain security features and digital data that verify authenticity. Document scanning uses high-resolution imaging and UV/infrared light to check holograms, microprint, and anti-forgery marks via OCR (Optical Character Recognition).

In particular, most passports and IDs today have embedded RFID chips readable by smartphones through NFC (Near-Field Communication), providing cryptographic verification that the document is genuine and unaltered. Combining physical document checks with chip reading is highly secure, because fraudsters can’t easily fake both.

This technology confirms the ID is real, untampered, and belongs to the presenter, delivering high-confidence validation.

Data and Device Analytics

Context matters in identity proofing. Thus, data analytics checks if information is consistent. For example: Does the phone area code match the address? Has the email appeared in fraud cases? Meanwhile, device analytics examines IP address (is the user coming from the location they claim, or a known proxy/VPN associated with fraud), device type, browser, geolocation, and access time to detect suspicious patterns.

For example, a New York applicant connecting from another country raises red flags. Machine learning models analyze hundreds of data points in real time, generating risk scores. This context-aware layer asks not just „what ID did you provide?” but „does this interaction look consistent and low-risk?” It catches account fraud that bypasses document checks and can fast-track low-risk users, acting as a silent fraud detector during signup.

Artificial Intelligence (AI) and Machine Learning (ML) Risk Engines

Today’s identity proofing is powered up by AI and ML, which are trained on millions of documents and fraud patterns. They are able to detect fake IDs through pixel-level analysis, spot deepfake videos, and combine multiple signals, such as document quality, biometric scores, and device risk, into real-time risk assessments.

For example, AI might flag a transaction where the document seems valid, but the device has fraud history, and the selfie appears suspicious. Machine learning improves continuously by learning from confirmed fraud cases, processing thousands of applications simultaneously in seconds versus hours manually.

While people are addressing transparency and bias concerns, AI-driven verification is becoming standard, making large-scale remote identity proofing both feasible and efficient.

Government and Third-Party Databases

Another pillar of identity proofing is connecting with trusted external data sources, which check government ID registries, credit bureaus, utility records, and watchlists to confirm information matches and the person isn’t synthetic or fraudulent.

Database checks validate that addresses exist, SSNs have history, and phone numbers are registered to the applicant. While not entirely reliable as they may be outdated, these records nonetheless add crucial consistency when combined with document and biometric checks.

Many countries offer digital ID verification APIs that instantly confirm identity details. These external sources act as electronic referees, vouching for data legitimacy and flagging discrepancies for investigation, strengthening overall identity proofing.

Reliable digital ID can make it easier, cheaper and more secure to identify individuals in the financial sector. Federal Reserve Bank of Atlanta

Challenges and Compliance in Identity Proofing

It’s no easy task to balance strict identity checks with privacy, fight new forms of fraud while avoiding bias, and navigate a web of regulations. Let’s discuss some of the key challenges and compliance issues.

Data Privacy

Because identity proofing handles highly sensitive personal and biometric data (passport scans, biometrics, ID numbers), global regulations, like the EU GDPR, and CCPA, lawful processing, explicit consent, and data minimization. Organizations must encrypt and securely store all proofing data and delete it when no longer needed. Some services perform real-time checks without storing copies to reduce risk.

The challenge here is balancing security needs with privacy rights while maintaining user trust through careful, compliant data handling.

Deepfakes and Synthetic Identities

Another alarming trend is AI-generated deepfakes that are used to fool video verification and create synthetic identities – fictitious personas using mixed real and fake data. A recent study found 75% of organizations experienced deepfake fraud attempts, while synthetic identities account for over 80% of new account fraud in some sectors, costing billions annually.

Serious threats like these require layered defenses: liveness detection, device reputation analysis, behavior patterns, and consortium data sharing. However, it’s an ongoing cat-and-mouse game as fraudsters constantly develop new tactics, which only underscores the importance of continuous innovation.

Algorithmic Bias

AI-powered identity proofing, especially facial recognition, is unfortunately prone to demographic bias. NIST studies discovered that some systems were up to 100x more likely to misidentify Asian or African American faces than white faces, often due to imbalanced training data. Of course, this causes unfair outcomes like higher rejection rates for certain groups.

The industry is addressing this through diverse datasets, bias testing, human oversight, and emerging standards. Ensuring equitable treatment across all demographics is essential for user trust and system reliability.

Regulatory Compliance

Identity proofing must satisfy multiple regulations and a variety of legal standards. Thus, KYC/AML laws require financial institutions to verify identities using reliable sources, privacy laws mandate consent and data protection, and standards like NIST 800-63A define identity assurance levels. And non-compliance leads to substantial fines.

Global regulators are pushing secure digital identity systems, especially for remote verification.

- FATF Recommendation 10 – requires verifying identity using reliable, independent sources.

- NIST 800-63A – defines Identity Assurance Levels (IAL1–IAL3) for proofing rigor.

- GDPR and eIDAS – set rules for data handling and electronic identity verification in the EU.

Even though navigating this complex maze of obstacles is challenging for identity proofing efforts, compliance is still the best means to ensure security and build customer trust.

Benefits of Identity Proofing for Businesses

Now let’s put a business hat on and answer the question: why should organizations invest in strong identity proofing? What’s in it for them and their customers? It turns out, if done well, identity proofing brings numerous benefits that improve the bottom line and overall brand success.

Regulatory Compliance

To comply with mandatory KYC, AML, and age verification laws and to avoid massive fines, businesses must implement identity proofing. Also, compliance spurs business opportunities, such as licenses to operate in regulated sectors, entry to new markets, and launching regulated products.

Moreover, it protects businesses from facilitating crimes like money laundering. A robust proofing process provides audit trails demonstrating required verification steps, keeping companies in good standing – all crucial factors for finance, healthcare, and other sensitive industries.

Customer Trust

No matter if it’s a financial platform, a marketplace, or a social network, strong identity proofing program signals that a business takes security seriously, and this boots customer trust, because users feel safer knowing fake accounts and fraudsters are kept out.

All reputable companies are expected to do customer due diligence. And even though a business requesting a person’s identity verification may seem like a hurdle, ultimately it builds trust. Verified identity information also streamlines account recovery and support.

Reduction of Fraud and Financial Loss

Proofing also prevents fraudsters from using fake identities or impersonating others, thus reducing losses from credit card fraud, loan defaults, and account takeovers. After all, stopping fraud at the gate is far cheaper than chasing it afterward. And strong proofing blocks schemes relying on weak onboarding and reduces operational costs: manual reviews, chargebacks, and support tickets.

Importantly, companies can enjoy strong ROI by improving fraud detection, and blocking synthetic identity fraud alone can save tens of thousands per loan, making robust proofing essential across all business sizes.

By augmenting organisations’ fraud-prevention capabilities, identity verification services help to minimise financial losses, increase customer confidence and loyalty and streamline compliance with KYC rules and other industry regulations. Adam Payne, Identity & Fraud Product Manager, Experian

Improved User Experience

If done right, modern digital identity proofing is faster and more convenient than in-person verification or mailing documents. Poor implementation causes abandonment of digital signups – often because it takes too long or overly complicated steps.

That’s why streamlined proofing that uses auto-capture, database lookups, and progressive profiling increases conversion rates. Verified users also enjoy benefits like faster transaction approvals (authentication) and fewer interruptions. In a nutshell, effective proofing balances security with ease, boosts sign-up completion and retention, and offers smoother user experiences.

Brand Reputation Protection

Platforms with fake accounts and fraud, lose both users and their reputation. And verified platforms are seen as safe spaces that users can trust – this is especially important for marketplaces and dating sites.

That’s why strong identity proofing prevents crises like press headlines about money laundering or bypassed age checks. Also, it provides better analytics, ensures ad spend isn’t wasted on bots, and reduces fraud investigations and support issues. After all, a verified user base is simply more valuable, creating positive feedback for business success.

Proofing is a Business Imperative

Although identity proofing usually works quietly behind the scenes, in essence it’s the foundation of digital trust, ensuring that every account starts with a verified, legitimate identity.

With fraud on the rise and regulations tightening, investing in strong identity proofing is essential. By combining biometrics, AI, and information intelligence, organizations can make onboarding seamless and secure, turning “prove you’re you” into a fast and trustworthy experience.

FAQ